Preferred Triple Threat

Destra Capital

April 1, 2021

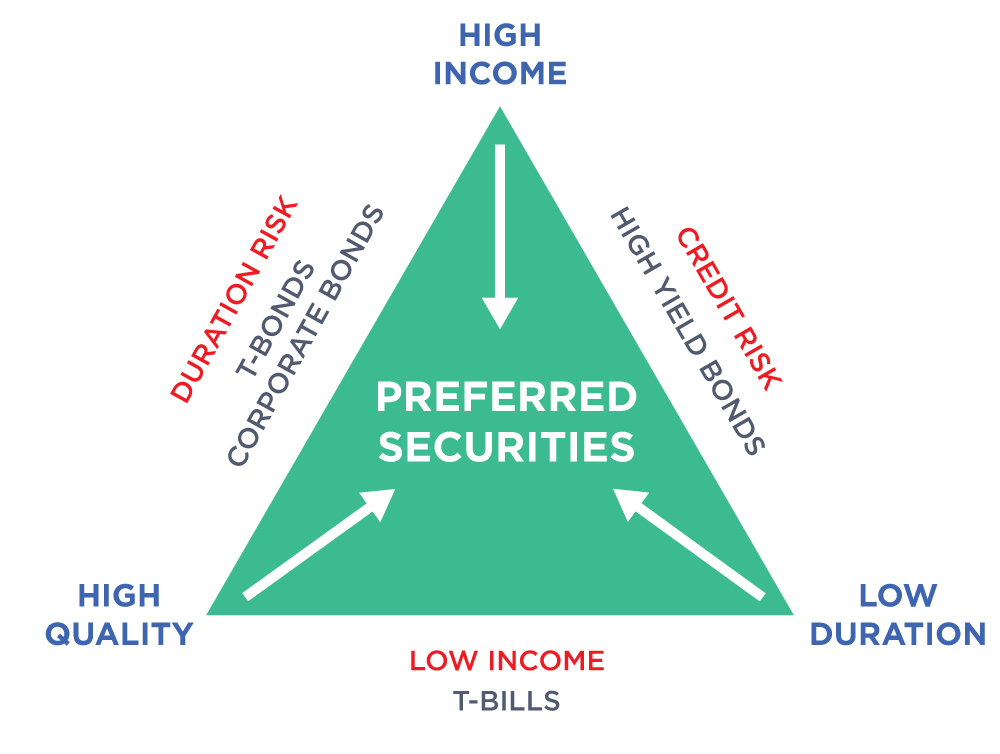

High Income

Yield is difficult to find in a low-rate environment, but Preferred Securities/Contingent Capital Securities (“CoCos”) continue to offer a yield advantage over many alternatives.

Preferreds are yielding about the same as high yield bonds, in the ballpark of 5% today.

And many Preferred securities pay Qualified Dividend Income, or QDI, that is taxed at a lower rate than ordinary income – either 0%, 15% or 20% depending on the taxpayer’s income and filing status.

Credit Strength

Credit Quality remains a bright sport for many of the issuers of preferreds – notably banks and financials, which have fared much better than normal in a significant recession and have shown major improvement in bank credit quality since the Global Financial Crisis.

In general, banks and other financial issuers were out in front of loan losses related to COVID-19 – adding aggressively to reserves in the first half of 2020 while adjusting operations to continue serving customers and earning a profit.

Moreover, no bank failed its stress tests undertaken by the Federal Reserve, even under the most adverse scenario. Given current capital strength and an improved economic outlook, many banks resumed modest share repurchases in 2021.

Intermediate Duration

With the recent modest uptick in interest rates and inflation fears on the table, several characteristics of Preferreds offer an attractive balance among duration risk, call risk, and reinvestment risk.

Fixed-floating and floating-rate Preferreds are among the highest yielding low duration securities. Their floating-rate features provide some insulation against a broad rise in interest rates. Additionally, fixed-float preferreds have typically had longer call protection which is critical for protecting income in a low yield environment where most preferreds trade above par value and the likelihood of call is high. With a longer runway to amortize price premiums, many fixed-float preferreds can move higher in price if the low yield environment persists.