SOFR, so Good! Transitioning away from LIBOR

Destra Capital

August 1, 2019So far, the transition from the London Interbank Offered Rate (LIBOR) to the Secured Overnight Financing Rate (SOFR) has been going smoothly.

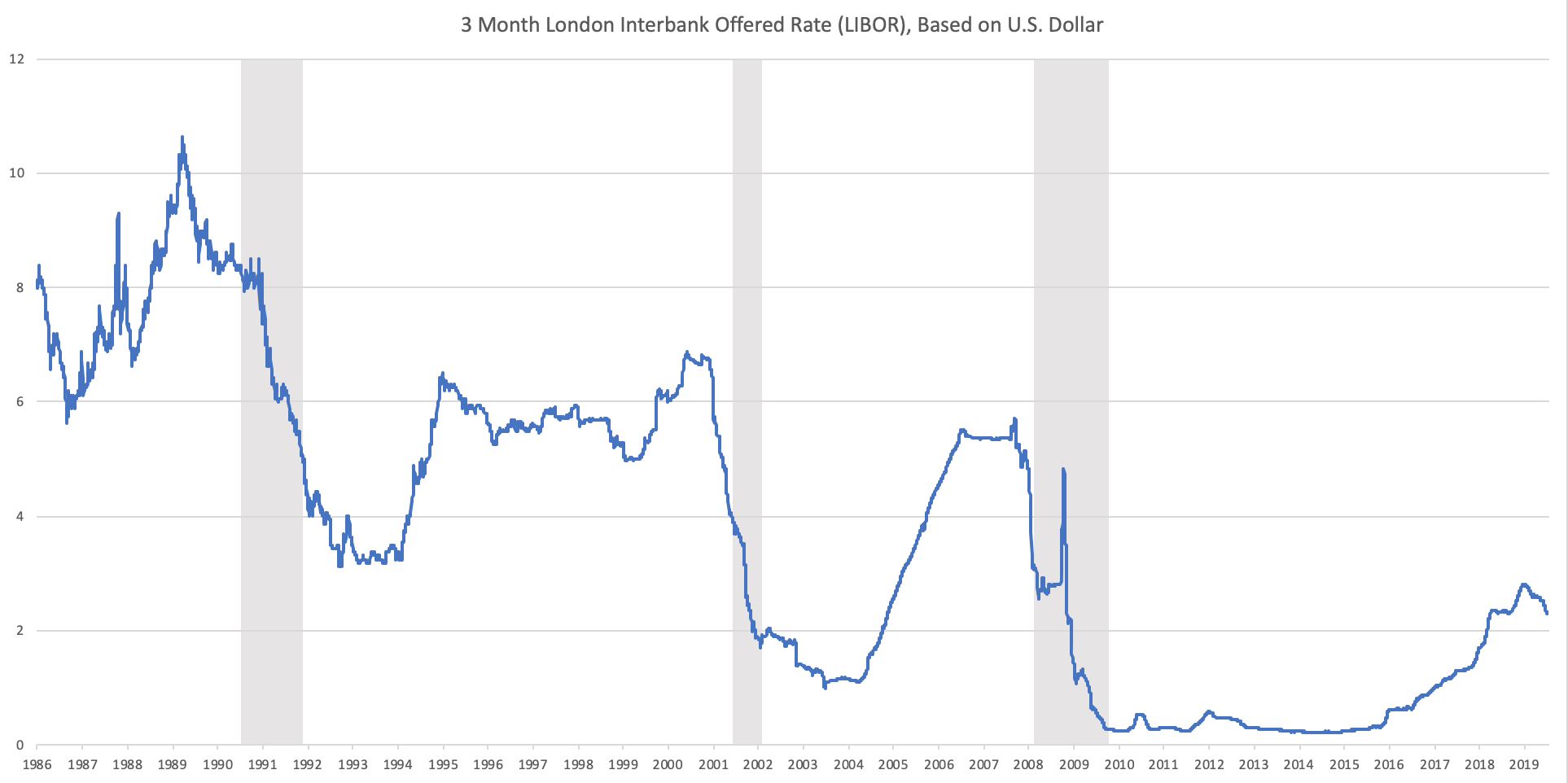

LIBOR is a floating rate benchmark that is widely used as a reference for setting the basic rate of interest that global banks charge one another on the interbank market for short-term loans. The rate is calculated and published each day by the Intercontinental Exchange (ICE). Prior to the Intercontinental Exchange providing administration for LIBOR, there had been much regulatory scrutiny regarding major banks attempting to manipulate and rig the LIBOR rates.

Libor has historically been used for different purposes: as a benchmark rate for (nearly all) derivative instruments, and for cash bonds with specific features such as floating rate notes and asset backed securities. In terms of derivative markets and cash bonds, we do not expect much disruption from the shift away from Libor to other money market rates.

Most of the subordinated debt that has been issued by banks in the past few years contains fallback language in the prospectus that makes the determination of a new floating rate the responsibility of the payment agent or the issuer. In the primary market for sub debt, Angel Oak has recently been requiring additional language that allows the rate selected by the payment agent or issuer to be overridden if deemed inappropriate by most investors. In almost all instances, the fallback language allows a spread to be added to the replacement rate to ensure that it is adjusted to be equal to the prevailing LIBOR-based coupon on the date that any new rate becomes effective. This should ensure that there are no discontinuities in the rates paid to investors after the change.

The Financial Service Authority (FSA), chief regulator of the financial services industry in the United Kingdom, announced that after 2021 banks will no longer be required to submit data reflecting their borrowing rates in the interbank market, which are instrumental in determining LIBOR.Currently, many of the outstanding cash market and derivative transactions are tied to LIBOR and are not expected to mature prior to the termination of LIBOR on December 31, 2021. Complicating matters, current fallback language in the deal documentation is not specific about which rate should be used to replace LIBOR in many of the outstanding transactions mentioned earlier.

We are closely monitoring the transition away from LIBOR since some preferred securities have LIBOR-based floating rate formulas. However, the preferred market is only one of many that will be impacted by the end of LIBOR. While the end of LIBOR is more than two years away, a solution is necessary (and expected) for a broad array of products. Ultimately, we are still in wait-and-see mode, but we remain confident that our market will settle on acceptable alternatives to LIBOR for both new and existing securities.

While we’re interested to see how this change may effect global yields in various related products or markets as the transition progresses, our current view is that this is mainly a non-event for our direct alternative institutional investments. Several of our underlying managers are affected, but in each case thus far, our discussions with them on the topic have left us highly confident in their ability to manage to it successfully. Through both these direct and indirect capabilities, any subsequent inefficiencies may actually be a positive, as it breeds potential opportunity to take advantage.

On November 17, 2014, the Federal Reserve assembled the Alternative Reference Rates Committee (ARRC) to accomplish four main objectives. These objectives were to:

- identify best practices for alternative reference rates,

- identify best practices for contract robustness,

- develop an adoption plan, and

- create an implementation plan with metrics of success and a timeline.

Through these objectives, the focus of the ARRC was to determine a replacement rate for USD LIBOR transactions.

While it will take time, the transition has already started and, from BlueBay’s point of view, it has so far been fairly rather frictionless. We are already primarily using ‘overnight index swaps’ instead of the traditional interest rates swaps which had been based on Libor. OIS rates and SOFR rates are based on the same concept of a secured lending rate and are trading close to repo rates. In the cash bond market, we are embracing the changes and do not foresee any major disruptions for our fixed-income portfolios going forward. On floating rates notes, while they have historically been issued with a spread to Libor, they are now more commonly issued with a spread to SOFR.

Both senior secured loans and the underlying financing for CLOs are both LIBOR based. The goal for the senior secured loan and CLO market is for both asset classes to shift away from Libor in tandem given CLOs represent over 50% of the buyer base in the senior secured loan market. The legal documentation for both asset classes now incorporate this eventual shift. There is still 2 ½ years until Libor is replaced so the markets have significant amount of time to properly make the shift.

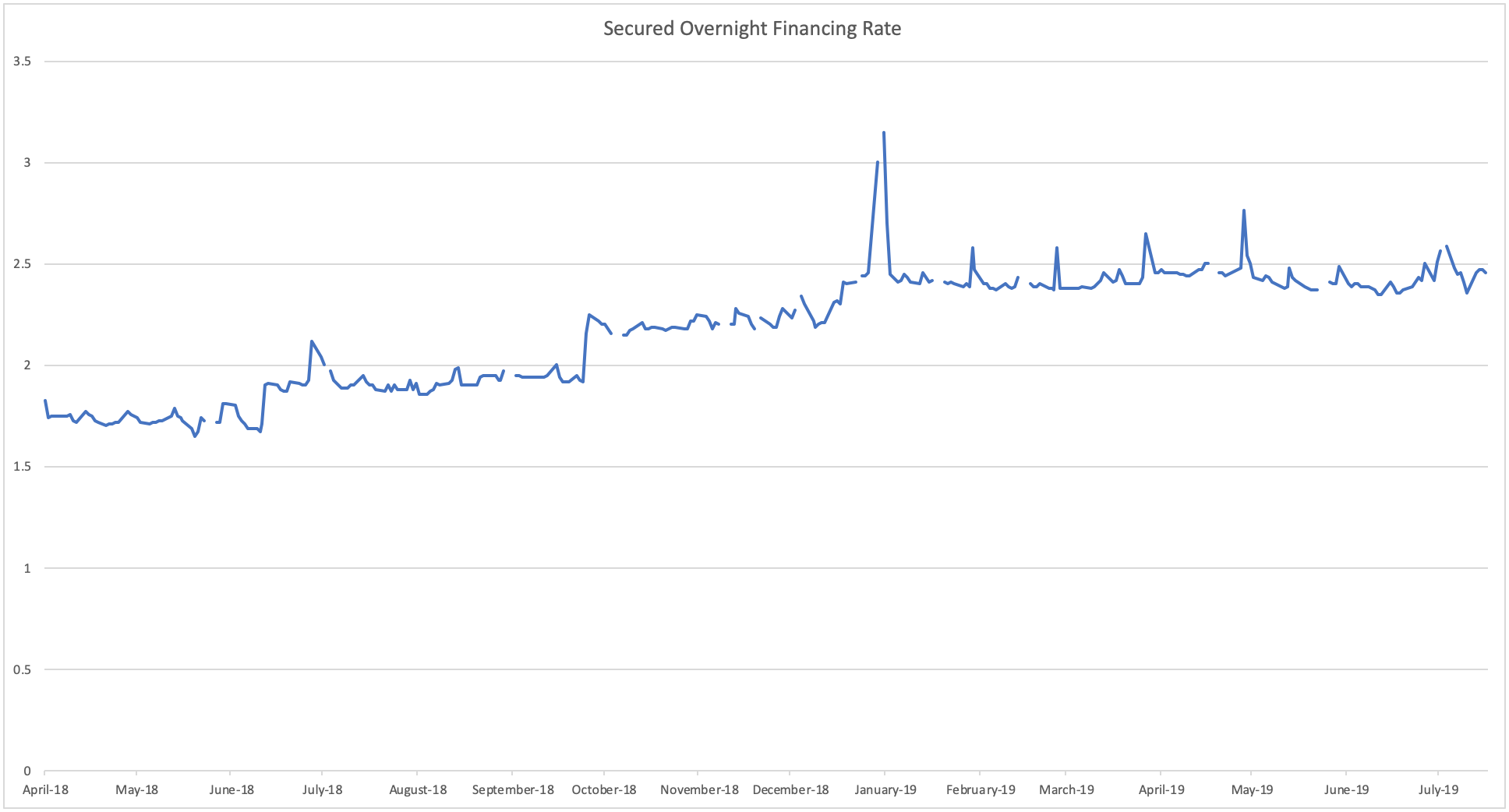

On June 22, 2017, the Alternative Reference Rates Committee identified the Secured Overnight Financing Rate (SOFR), as the rate that represents the best practice for use of US dollar derivatives and other financial contracts. The committee considered a comprehensive list of potential replacements, but ultimately determined that because of its range of coverage, SOFR will properly represent the conditions of the overnight Treasury repo market and provide the best benchmark for setting terms and rates to replace LIBOR. Some issuers of securities and derivatives have already begun to utilize this new overnight rate in recent deals.

Source: ARRC Second Report, 4/15/19

Source: https://fred.stlouisfed.org/series/SOFR

With the termination of LIBOR calculation just two years out, many asset management firms and other capital market participants have begun to transition from LIBOR. For more information on the transition from Libor to SOFR and how it may effect investments represented by Destra, please contact us. We will also continue to keep you abreast of developments as the transition continues, …..SOFR, so good!

Investors in bank sub debt are not expected to be impacted materially by this change because for the first five years after issue the notes are fixed rate. After a five year lock-out period the notes become callable and also floating rate. However, the notes also begin to lose their regulatory capital treatment in a step-down fashion each year until maturity. Banks will therefore be heavily incentivized to call the debt regardless of the prevailing rate environment and reissue new sub debt to maintain their regulatory capital requirements.

About Destra

Destra Capital is a boutique Investment Management firm that partners with independent, institutional investment managers that have developed innovative and specialized investment strategies. Headquartered in Chicago, IL, Destra was Founded in 2008 by a senior management team with decades of knowledge and expertise in the industry driven by the guiding principle of providing Responsible Alpha® to the wealth management marketplace through investment products offered by Destra.

Common to many of Destra's investment offerings is the goal of providing market leading returns with an eye towards managing downside risk -- we call this Responsible Alpha®. Our experience working with the wealth management marketplace shows investing is not about periodic outperformance, but rather it is about consistent, steady returns over time. This is how true wealth is produced, preserved, and prolonged. The pursuit of Responsible Alpha® is the guiding principle to the investment products Destra offers.

Destra Capital Advisors LLC is an SEC registered investment advisor and the advisor to the Destra Funds. Destra Capital Investments LLC is a FINRA registered broker dealer and distributor to Destra Funds and other investments.