The Ice Man Cometh

Destra Capital

Credit markets started 2024 by scattering in all directions! The market euphoria that ended 2023 ended over the New Year’s weekend as well. The Destra Credit Strategies Indicator (“CSI”) tracks 18 different sub-strategies of credit investing. 6 posted negative returns in January, with International Investment Grade down the most at -1.30%, while 12 of the CSI sub-strategies were positive in the month with Preferreds, the big winner, up +2.55%. The irony, that many European style preferred instruments, often called CoCos, are issued by “investment grade” banks should not be lost on market observers.

Convertibles, International High Yield, Mortgage Backed Securities, Municipals, and Emerging Market Debt joined International Investment Grade on the negative side of the ledger in January.

Negative Performing Sub-Strategies in the CSI

| Municipals | -0.14% |

| Mortgage Backed Securities | -0.40% |

| Emerging Market Debt | -0.44% |

| Convertibles | -0.87% |

| International High Yield | -1.00% |

| International Inv Grade | -1.30% |

Source: Destra Capital, Morningstar as of 1.31.24

On the positive side, the divergence between US High Yield and US Senior Loans continued, with the bonds flat at +0.06% but the loans moving up nicely at +0.52%. If the Fed pivot is in the front windshield, you might expect that the relatively modest duration of a high yield bond would be more attractive than the 0 – 90 day duration of a loan that resets, but the market does not seem to agree.

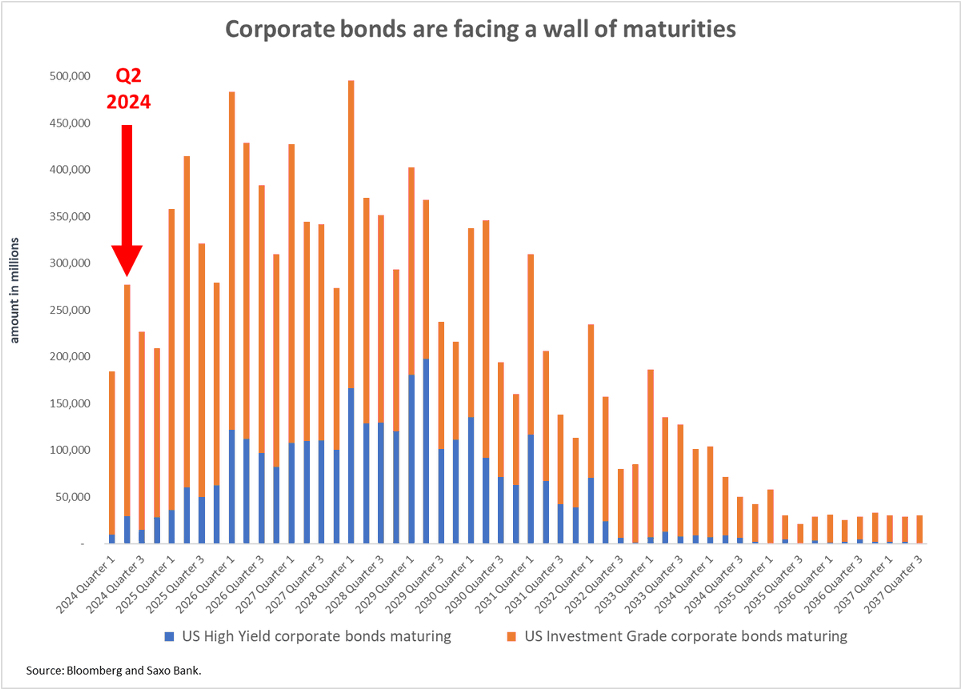

Refinancing all that leveraged debt is gonna be tricky in 2024 and beyond. According to Althea Spinozzi, Head of Fixed Income Strategy at SaxoBank, “Roughly $276bn (IG+HY) corporate bonds need to be refinanced in Q2 2024 Despite the recent bond rally: HY must refinance from an avg coupon of 5.8% to 9%. IG must refinance from an avg coupon of 3.77% to 5.75%, the highest since Q3 2007 (excluding Q3 '23 peak of 5.79%)”

All In All, Just Another “Refinancing” In the Wall

Positive Performing Sub-Strategies in the CSI

| Preferreds | 2.55% |

| BDCs | 1.54% |

| Event-Driven Credit | 1.05% |

| Interest Rate Hedged | 0.94% |

| Structured Credit Senior | 0.88% |

| Emerging Markets High Yield | 0.56% |

| Senior Loans | 0.52% |

| Structured Credit Junior | 0.48% |

| Municipals High Yield | 0.41% |

| CMBS | 0.38% |

| US Investment Grade | 0.26% |

| US High Yield | 0.06% |

Source: Destra Capital, Morningstar as of 1.31.24

Beyond Preferreds remarkable start to the year, BDCs and Event-Driven Credit strategies notched returns over 100 bps each for the month. BDCs were up +1.54%, while EDCs returned 1.05%.

Federal Government Debt : Mortgaging Away The American Future

Credits were not the only fixed income category to have bifurcated results to start 2024. The supposedly credit-risk free US Treasury markets saw pretty wide performance difference as well, with Long Treasury strategies getting absolutely crushed, down -2.20% for the month, while Intermediate and Short Treasury strategies were up modestly in the 20 – 30 bps range.

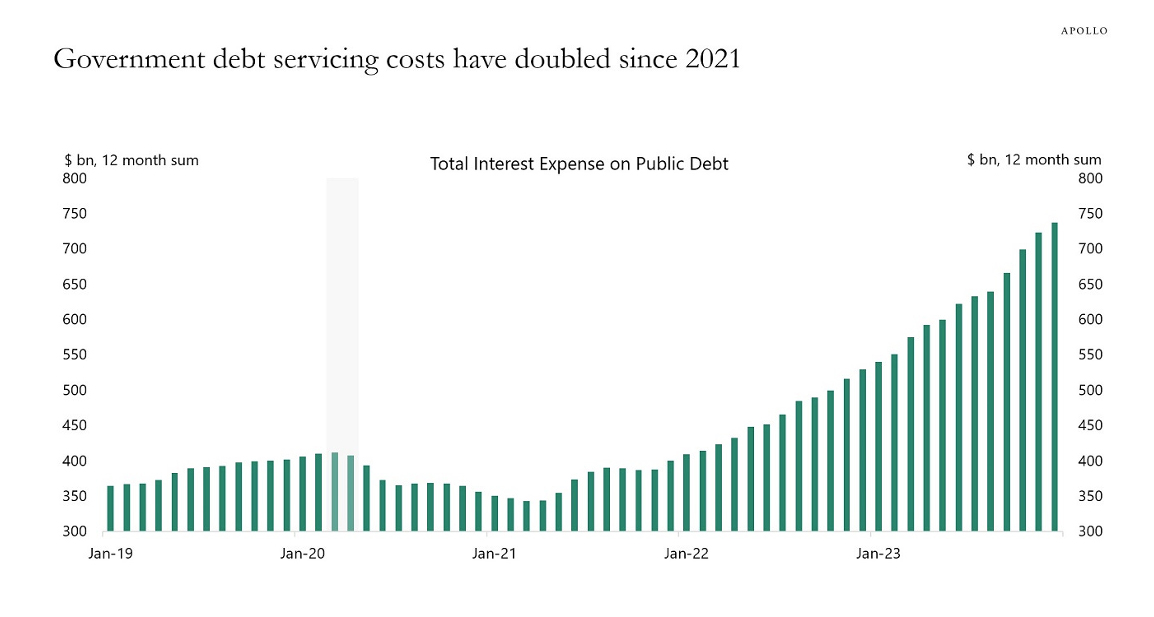

Irrespective of where the Fed takes interest rates in 2024, it is becoming undeniable that the exploding debt of the Federal government will have major effects on finance, politics and society. According to Torsten Sløk, Chief Economist at Apollo, the interest payments on US Government debt have doubled since 2021. That is a harbinger of bad things to come.

Source: Apollo Global Management, https://apolloacademy.com/government-interest-payments-have-doubled-since-2021/

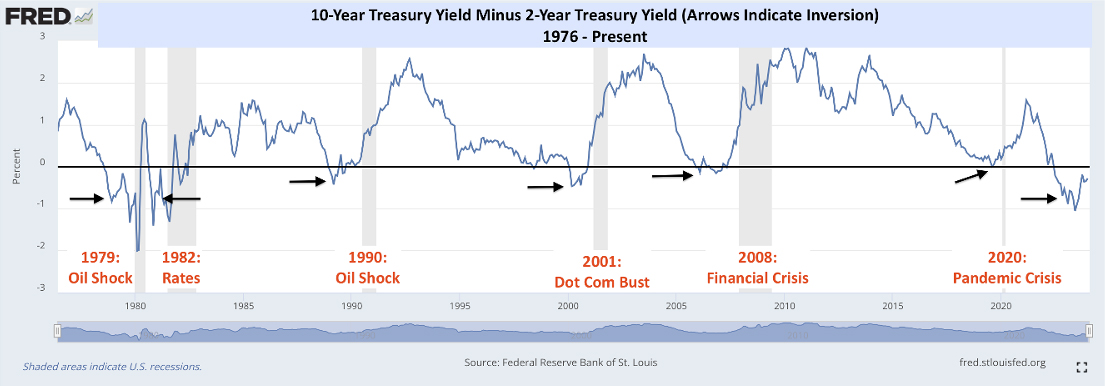

Yield Curve Inversions, Be Careful What You Wish For

And speaking of bad things to come, in the last four yield curve inversions, going back to the late 1980’s, the curve passed back into normal, positive sloped territory prior to the economy officially entering a recession. With the bull steepening that the curve has been experiencing in the last few months, we might be approaching a switch back to a normal slope and that just might be the last warning before the recession. Be careful what you wish for?

Source: Federal Reserve Bank of St.Louis, https://fred.stlouisfed.org/series/T10Y2Y

February is the month that loves bonds! Cupid is for debenture seekers and income romantics. Will we be back next month to let you know if it was all rose petals and chocolates for credit markets in February.